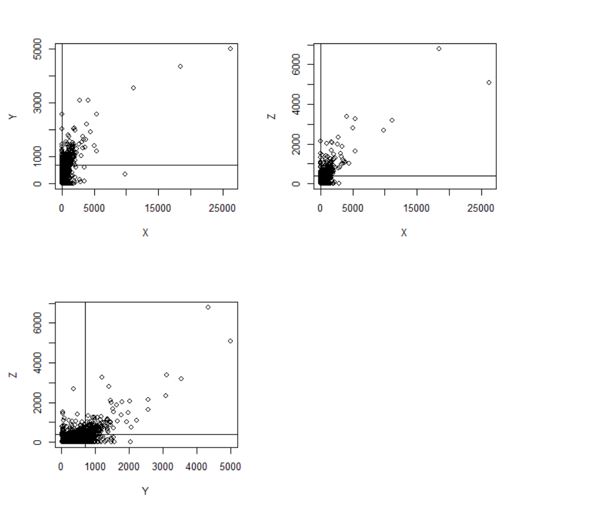

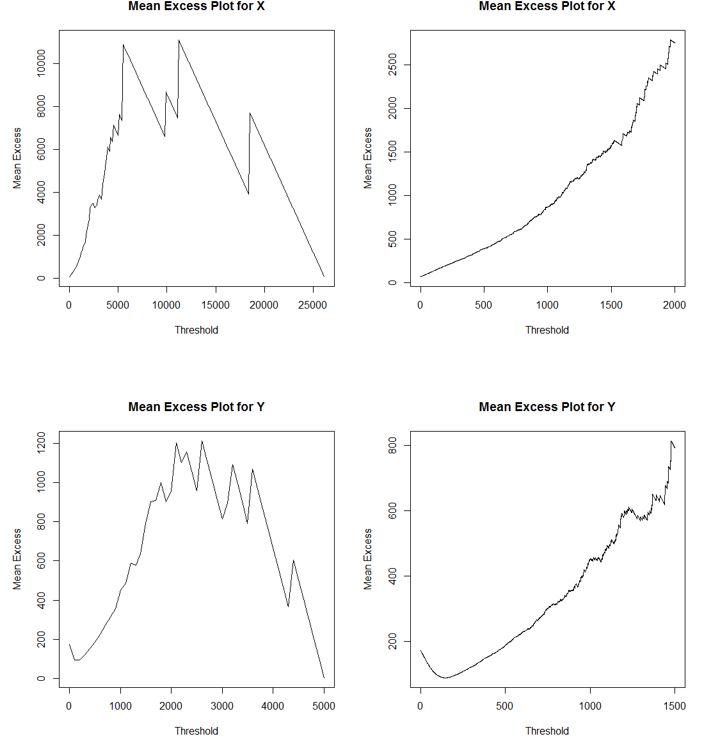

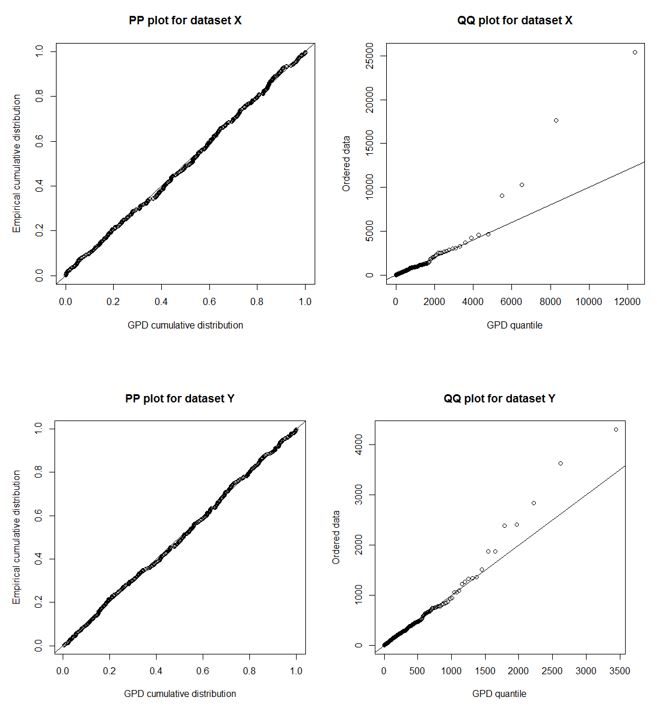

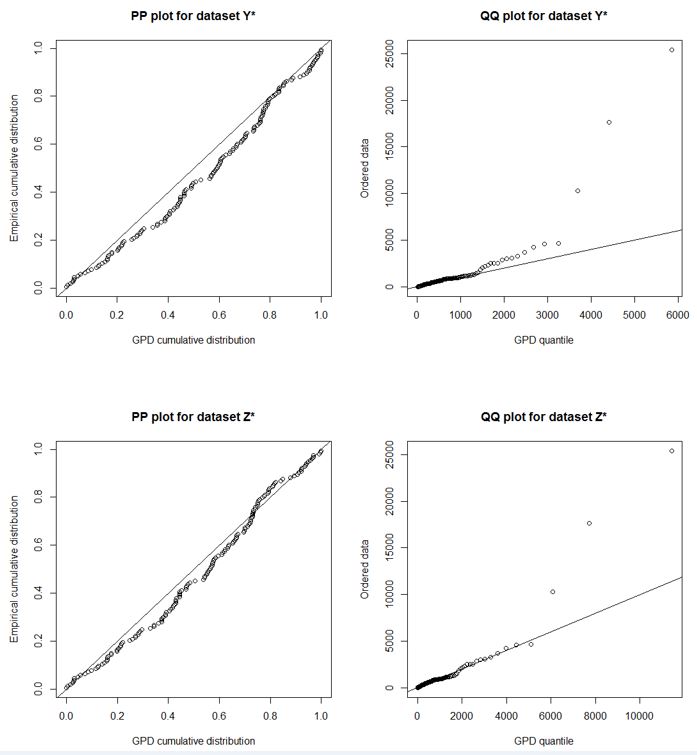

In recent years, extreme value theory (EVT) has been a popular topic not only in traditional natural science fields such as hydrology, but also in the finance and insurance industries. In summary, EVT can be considered as a general tool to model extreme or rare events such as a 1 in 100 year flood or a 1 in 1000 year economic stress scenario. Even though EVT is a great theory to model extreme scenarios, apply the EVT can sometimes be difficult especially in the multivariate setting due to the loss of natural ordering in a multidimensional space. This term paper focuses on how to apply the peaks-over-threshold (POT) method of EVT in both the univariate and multivariate settings. The univariate problem focuses more on details of how to apply the POT method, while the multivariate problem focuses on how to capture the positive tail dependence structure using an extreme-value copula. Both problems use the same simulated dataset which is high-dimensional and heavy-tailed.

Modelling extreme data is usually very challenging, and one of the main reasons is that there is usually not enough data to train the models. The data scarcity problem gets even worse in high-dimensions as it is even more difficult to define what is an extreme data. From past experience, I did find it that in high dimensional setting, use a copula model is usually the best choice and which copula family to use sometimes has little impact on the result (which is surprising sometimes from a theoretical point of view).

Last updated on Jan 1, 2019